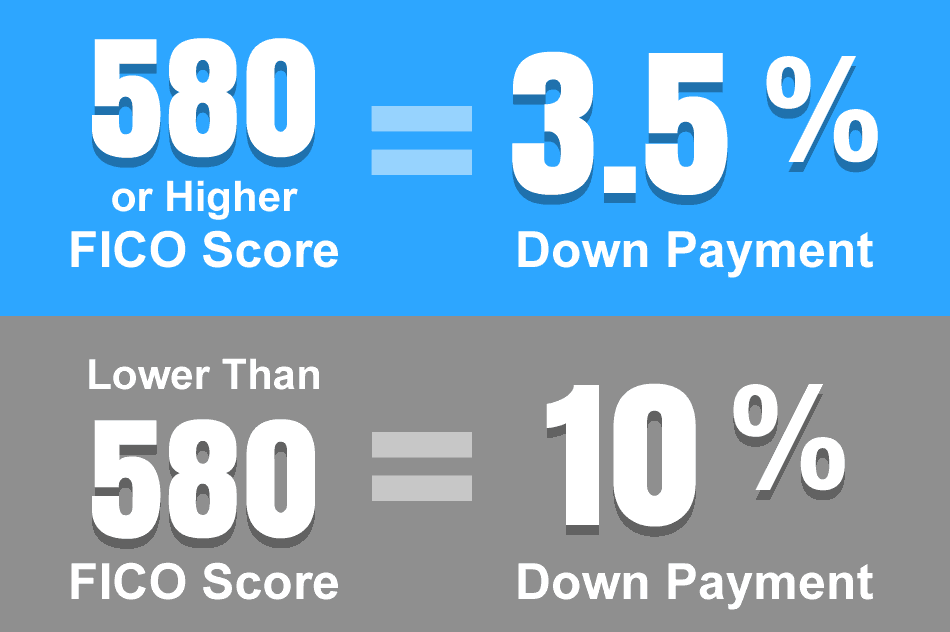

These loans do require evidence of transfer and the donor should show the source of the funds for the present. FHA home mortgages have low deposits (3. 5%), and deposit gifts can come from timeshare deals household members or buddies. These loans do need evidence of transfer and the donor must prove the source of the funds for the gift.

If you have any questions at all, just connect! I'm here to help make the loan procedure a smooth one for you and can assist you and the giver understand precisely what to do.

Purchasing a house is pricey nowadays, and numerous people require a little help to come up with an adequate down payment. If you do, you may have heard something about a crucial file called a mortgage present letter. Here's whatever you require to know if you're being given funds to approach your new home's deposit.

This is really not true. Utilizing gift cash for a down payment isn't as cut-and-dried as it appears. The source of the money in your savings account matters simply as much as the cash that's really because account. The bank needs to be able to see exactly where the deposit came from before you can use it to close on a home.

After you've made an application for a mortgage, an underwriter takes your total application and goes through your financial info to make sure you in fact get approved for the loan. Generally, the underwriter is choosing how risky it is to lend you the cash you're looking for. The underwriter will take a look at your income, credit score, and your possessions to determine your value for a loan.

Regular month-to-month deposits from incomes are quickly explained, but anything large and unexpected will need to be taken a look at more carefully. A bank needs to take a look at any big quantities of cash that were offered to you to make certain financing you cash is an excellent choice. If the deposit funds in your account were a loan, you 'd have the extra monetary stress of that loan, and this would make it less likely that you could pay the home loan back.

A gift letter is written by the giver to discuss that you do not need to pay the cash back to them, but it also includes a few other crucial details. Here are the primary things the letter must consist of: The address of the home you're purchasing The donor's contact info The donor's relationship to you The specific quantity and date of the present A declaration that you don't need to pay back the money A signature Depending upon the loan and the situation, a gift letter might not be sufficient paperwork for these talented funds.

The 5-Minute Rule for Why Do Banks Sell Mortgages To Other Banks

Make sure that you and the donor keep a strong proof for the cash being gifted to you. For instance, keep records of get rid of timeshare legally stock sales, deposit slips, checks, and bank declarations. If you are receiving several down payment presents, make sure to follow the process specifically for each present.

This is specifically true for government-backed loans. For example, VA loans, which are available to active and seasoned members of the U.S. military, do not require a down payment at all, so any or all of the money can come from presents. The requirements for showing the source of these funds tend to be more lax, as well.

These loans do need evidence of transfer and the donor must prove the source of the funds for the present. FHA home mortgages have low down payments (3. 5%), and down payment presents can come from Homepage relative or buddies. These loans do need evidence of transfer and the donor need to show the source of the funds for the gift.

If you have any concerns at all, just reach out! I'm here to help make the loan procedure a smooth one for you and can assist you and the giver know precisely what to do.

A gift letter is a piece of legal, written correspondence clearly stating that money gotten from a pal or relative is a gift. Present letters for tax purposes typically enter play when a debtor has actually gotten assistance in making a down payment on a new house or other realty home.

A present letter is a piece of legal, written correspondence clearly specifying that cash gotten from a buddy or relative is a present. Present letters are essential when it comes to paying a genuine estate deposit, for example, due to the fact that lenders tend to discredit debtors using extra borrowed money for a down payment on a home or other residential or commercial property.

For 2020, the IRS announced that the estate and present tax exemption is $11. 58 million per person. what are reverse mortgages and how do they work. Present letters are crucial since, in general, loan providers tend to frown upon debtors using extra borrowed cash for a down payment on a home or other home. "Talented" cash, nevertheless, is a different story.

Some Known Details About How Do Adjustable Rate Mortgages Work

The gift-giver needs to straight compose the letter for it to have any credibility. The letter also often reveals the relationship between the gift giver and receiver. A present can be broadly defined to include a sale, exchange, or other transfer of residential or commercial property from one individual (the donor) to another (the recipient).

Several gifting techniques rest on gift letters. For instance, inter vivos gifting happens while an individual is still alive and can minimize the taxable estate considering that the private no longer owns the property when they pass away (although inter vivos gifts might still undergo taxes if made 3 years prior to that individual's death).

This omits its present worth from the donor's estate and likewise eliminates future appreciation from the estate. On the other hand, gifting possessions that have currently increased significantly in value is less helpful, as the recipient will have the very same tax basis (carryover basis) in the residential or commercial property as the donor. If the recipient were to acquire the asset instead of receive a gift throughout the donor's life, the possession is stepped up to the fair market value of the home at the time of death.

Down payments are one of the most significant hurdles to buying a home. Fortunately, if you haven't saved enough of your own funds for a home purchase, lots of lending institutions allow customers to purchase a house with present funds. If a parent, sibling, or grandparent uses to present funds for your home mortgage costs, you may not believe to divulge this info to your lender.

Although lending institutions do allow gift funds, they also require mortgage candidates to divulge the source of these funds. Keep in mind, when requesting a home mortgage loan, the loan provider needs a clear picture of your monetary situation. This consists of information about your work, income, and assets. This is why a lender will ask for copies of your latest bank declarations.

However sometimes, a household member uses to pay these expenses as a present to you. Now you understand that you can use gifted funds to make your down payment, however who can those funds come from? Donor requirements differ by lender and home mortgage program. Some programs only permit presents from a blood relative, or in some cases, a godparent.