Traditional loans are frequently likewise "conforming loans," which indicates they meet a set of requirements specified by Fannie Mae and Freddie Mac two government-sponsored business that buy loans from lending institutions so they can give home loans to more individuals. Conventional loans are a popular option for buyers. You can get a standard loan with as low as 3% down.

This contributes to your regular monthly expenses however permits you to enter into a brand-new house faster. USDA loans are only for homes in eligible backwoods (although numerous homes in the suburban areas certify as "rural" according to the USDA's meaning.). To get a USDA loan, your home earnings can't go beyond 115% of the location typical income.

For some, the warranty charges needed by the USDA program cost less than the FHA mortgage insurance coverage premium. VA loans are for active-duty military members and veterans. how do mortgages work in ontario. Backed by the Department of Veterans Affairs, VA loans are a benefit of service for those who've served our nation. VA loans are a great option because they let you purchase a home with 0% down and no personal home loan insurance coverage.

Each monthly payment has four huge parts: principal, interest, taxes and insurance coverage. Your loan principal is the quantity of cash you have delegated pay on the loan. For instance, if you borrow $200,000 to purchase a house and you settle $10,000, your principal is $190,000. Part of your month-to-month home mortgage payment will automatically go toward paying down your principal.

6 Simple Techniques For Reverse Mortgages How They Work

The interest you pay every month is based upon your rate of interest and loan principal. The cash you pay for interest goes straight to your mortgage company. As your loan develops, you pay less in interest as your primary reductions. If your loan has an escrow account, your monthly mortgage payment may also consist of payments for property taxes and homeowners insurance.

Then, when your taxes or insurance coverage premiums are due, your lender will pay those bills for you. Your home loan term describes for how long you'll make payments on your home loan. The two most typical terms are 30 years and 15 years. A longer term generally suggests lower regular monthly payments. A shorter term usually implies larger regular monthly payments however substantial interest cost savings.

In a lot of cases, you'll need to pay PMI if your down payment is less than 20%. The expense of PMI can be added to your month-to-month home mortgage payment, covered via a one-time upfront payment at closing or a combination of both. There's also a lender-paid PMI, in which you pay a slightly greater interest rate on the home mortgage rather of paying the regular monthly charge.

It is the written guarantee or contract to pay back the loan utilizing the agreed-upon terms. These terms consist of: Rates of interest type (adjustable or repaired) Rate of interest percentage Quantity of time to pay back the loan (loan term) Amount obtained to be repaid in complete Once the loan is paid completely, the promissory note is offered back to the borrower.

The Greatest Guide To How Do Owner Financing Mortgages Work

The American dream is the belief that, through effort, guts, and determination, each person can accomplish monetary prosperity. Many people interpret this to indicate an effective profession, status seeking, and owning a house, a vehicle, and a household with 2. 5 kids and a dog. The core of this dream is based upon owning a home.

A home mortgage loan is just a long-lasting loan provided by a bank or other lending institution that is protected by a particular piece of property. If you stop working to make timely payments, the loan provider can repossess the residential or commercial property. Since houses tend to be pricey - as are the loans to spend for them - banks permit you to repay them over extended time periods, known as the "term".

Much shorter terms may have lower rates of interest than their similar long-term brothers. However, longer-term loans may provide the benefit of having lower month-to-month payments, due to the fact that you're taking more time to pay off the financial obligation. In the old days, a neighboring savings and loan might provide you cash to purchase your home if it had sufficient cash lying around from its deposits.

The bank that holds your loan is responsible mainly for "maintenance" it. When you have a home mortgage loan, your month-to-month payment will generally consist of the following: An amount for the primary amount of the balance An amount for interest owed on that balance Property tax Homeowner's insurance Home Home loan rate of interest can be found in numerous varieties.

The Best Strategy To Use For How Does Mortgages Work

With an "adjustable rate" the rates of interest changes based on a defined index. As a result, your monthly payment amount will vary. Mortgage been available in a range of types, including standard, non-conventional, fixed and variable-rate, house equity loans, interest-only and reverse mortgages. At Mortgageloan. http://reiduoaw481.image-perth.org/things-about-how-do-dutch-mortgages-work com, we can help make this part of your American dream as easy as apple pie.

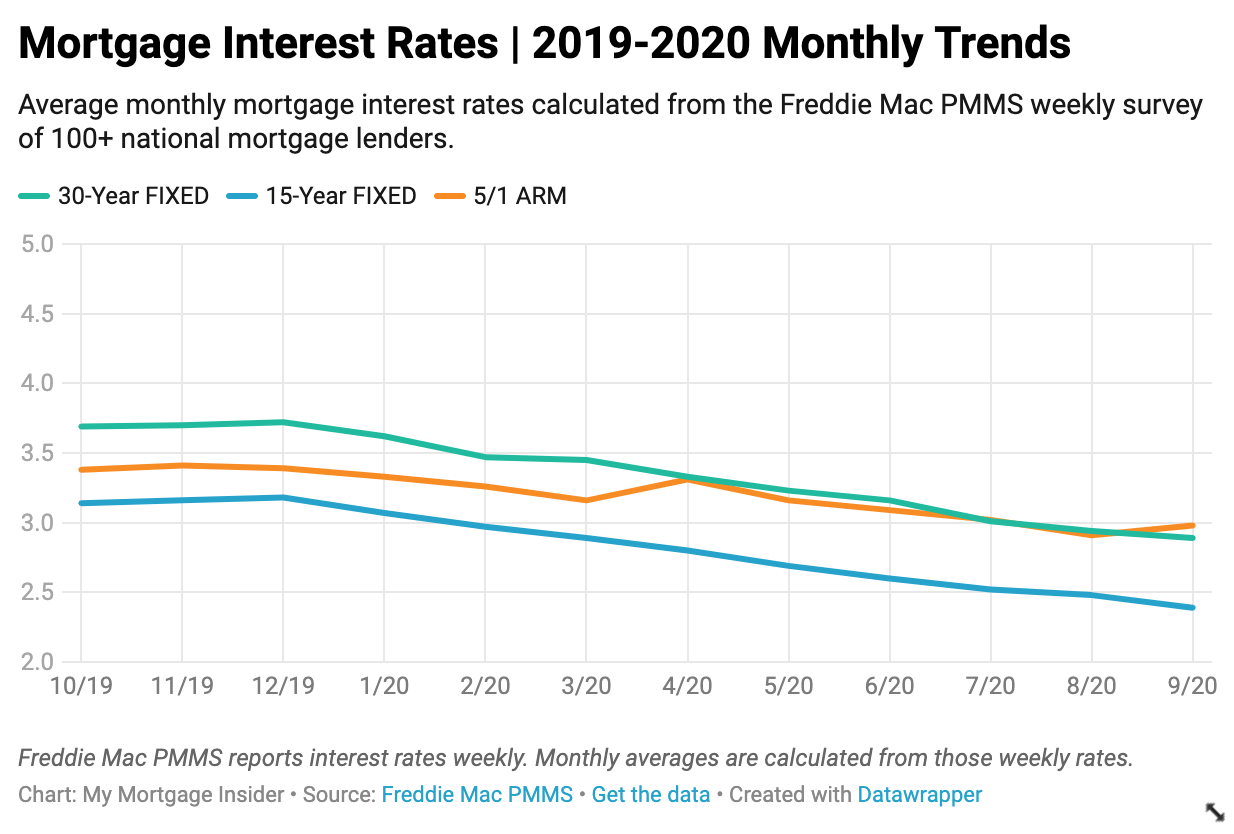

Probably among the most confusing features of mortgages and other loans is the computation of interest. With variations in compounding, terms and other aspects, it's tough to compare apples to apples when comparing home loans. In some cases it appears like we're comparing apples to grapefruits. For example, what if you desire to compare a 30-year fixed-rate home loan at 7 percent with one indicate a 15-year fixed-rate home mortgage at 6 percent with one-and-a-half points? Initially, you have to remember to likewise think about the charges and other expenses related to each loan.

Lenders are needed by the Federal Truth in Lending Act to disclose the efficient portion rate, along with the total financing charge in dollars. Ad The annual percentage rate () that you hear so much about allows you to make true contrasts of the real costs of loans. The APR is the typical annual financing charge (that includes fees and other loan costs) divided by the amount borrowed.

The APR will be slightly higher than the rates of interest the loan provider is charging because it consists of all (or most) of the other costs that the loan brings with it, such as the origination charge, points and PMI premiums. Here's an example of how the APR works. You see an advertisement using a 30-year fixed-rate home loan at 7 percent with one point.

How Do Mortgages Work In Portugal Things To Know Before You Get This

Easy choice, right? Actually, it isn't. Thankfully, the APR considers all of the small print. State you need to borrow $100,000. With either lending institution, that suggests that your month-to-month payment is $665. 30. If the point is 1 percent of $100,000 ($ 1,000), the application fee is $25, the processing charge is $250, and the other closing costs total $750, then the total of those charges ($ 2,025) is subtracted from the real loan amount of $100,000 ($ 100,000 - $2,025 = $97,975).

To discover the APR, you identify the rates of interest that would equate to a month-to-month payment of $665. 30 for a loan of $97,975. In this case, it's really 7. 2 percent. So the 2nd loan provider is the better deal, right? Not so quick. Keep checking out to discover the relation between APR and origination costs.