If you think a reverse home mortgage could assist you stay in your home with retirement, make certain you understand the threats and also benefits so you can make a better-informed choice. A reverse home loan can transform your home right into a constant supply of cash money, yet it can be costly and also lugs some threats. A Shared Recognition Home mortgage thinks about the recognition in value of your home in between the moment the financing is authorized and the end of the funding term. The lender gets an agreed-to portion of the appreciated value of the financing when the car loan is terminated. Prior to you decide to obtain a reverse home mortgage, make certain you take into consideration the pros and cons thoroughly.

- If you did spend the cash, you would certainly owe it as well as would start to build up interest owed accurate you did spend for as lengthy as it continued to be exceptional on the line.

- HECMs were developed in 1988 to help older Americans Learn here make ends meet by enabling them to use the equity of their homes without needing to vacate.

- Reverse home loans certainly satisfy a demand on the market, however they are not appropriate for all retirees.

The loan provider's threat is factored right into the rate of interest, settlement problems and certification process. You also have the option to obtain the proceeds of the reverse mortgage as a lump-sum settlement, planned developments to enhance your yearly income or a combination of these options. If this all seems a little also excellent to be real, you're best to do your research prior to identifying if a reverse home mortgage is a great choice for you and also your household. Personal home loan insurance or PMI is an insurance plan secured as well as paid for http://cruzekxh546.lucialpiazzale.com/8-sorts-of-mortgage-loans-for-customers-as-well-as-refinancers by a borrower for the advantage of the loan provider. It is essential that you go over the monetary effect of PMI with your lending institution as well as a housing therapist or lawyer prior to getting a reverse home loan.

One of the most popular type of reverse home mortgage is the FHA-insured Home Equity Conversion Mortgage. The insurance policy protects the lender, not the debtor. For some people, the charm of a reverse home loan is that you can access cash money for living expenditures and you don't make any type of month-to-month settlements to the loan provider or pay the passion until you offer your residence. If you're struggling to cover the various other costs of your home-- Among the crucial components of a reverse mortgage is your capacity to pay your property taxes and also house owners insurance policy.

Other Insurance

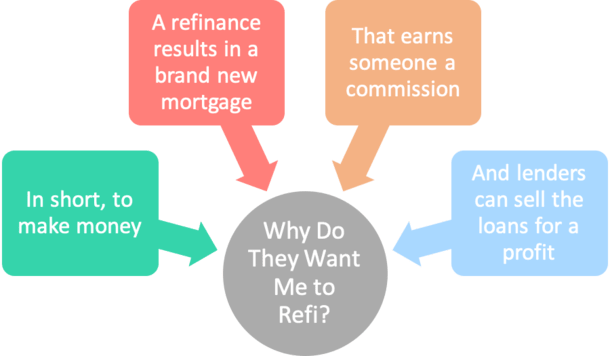

Chris- I would certainly suggest you have actually not properly sold your house with a reverse home loan. You can offer the residence, re-finance the residence, you can change instructions anytime. There are no manacles with the HECM, it merely provides you extra choices and flexibility if the conditions of your retirement require them. For anyone still bring an equilibrium, that most likely implies replacing an inexpensive home loan with something far more pricey. The justification for higher rates as well as charges on 2nd and also third home loan has actually historically been the higher danger from the key lien owner confiscating after default. It doesn't make any kind of feeling for the HECM lender to get all the extra benefits that include added danger when there is successfully no risk at all to making the loan.

That's a lot of cash just to access the equity in your very own residence. Reverse home mortgages included more laws than a routine mortgage so that make up some of the added fees. Because reverse home loans are so intricate, you'll require to meet with an expert who can clarify all your choices. HECMs are structured to ensure that both adjustable-rate and fixed-rate funding choices are readily available.

Explore All Your Choices

Nevertheless, if you're in a vendor's market you'll likely need to pay a costs for your new, smaller space. Even so, preserving your house equity without taking out a reverse mortgage can be a a lot more appealing-- and also less expensive-- way to cover costs in retirement. While a reverse home loan may seem like a great way to access cash in your gold years, it is necessary to comprehend the truths of this kind of lending. [newline] Right here's exactly how you can anticipate to benefit from a reverse mortgage-- as well as what to watch out for when comparing this lending choice to other options. The most significant threat with a reverse home mortgage is that the interest charges substance and also chip away at your equity.

Homeequity Financial Institution Clients Advise Their Chip Reverse Home Loan

I would believe that the majority of the moment your house isn't mosting likely to remain in the household. That's not necessarily a huge bargain; I do not desire my parent's house for instance, yet if it matters to you, attempt to see completion from the get go. In some ways, a reverse mortgage is additionally an annuity. It doesn't actually care about your gender or health and wellness status. It likewise doesn't guarantee to pay up until you pass away, even if Website link you select the period choice. It just assures to pay while you are staying in your house. [newline] There goes your residence as well as your "annuity" repayments.

Unlike a few other types of finances, income as well as credit report are ruled out for eligibility for a reverse home loan. Nevertheless, because of mortgage guidelines and regulations in Canada, you may be needed to send them. Some households may be able to avoid actually utilizing a reverse mortgage.

We continually strive to supply consumers with the specialist guidance and also tools required to prosper throughout life's economic journey. Bankrate's editorial team writes in behalf of YOU-- the visitor. Our objective is to give you the most effective advice to assist you make smart personal finance decisions. We adhere to rigorous standards to make sure that our editorial material is not influenced by marketers. Our content group receives no straight settlement from advertisers, and our material is extensively fact-checked to guarantee precision. So, whether you read a short article or an evaluation, you can rely on that you're obtaining credible and dependable details.